Demographic & Market Analysis

Understanding regional demographics is key to this study. Population and median household incomes for the region and in the neighborhoods impacted by the grocery store closures highlight critical issues for business sustainability. Retailers are constantly assessing regional market conditions for proposed and existing stores utilizing market data.

Researchers with University of Illinois Extension collected and analyzed demographic and market data relevant to the areas impacted by the stores closures. The researchers analyzed data at the census tract level of the Southside and East Bluff neighborhoods likely to have been impacted the greatest by the recent Kroger closures. They also included analysis of the cities of Peoria and East Peoria, as well as Peoria, Tazewell and 10 surrounding counties to put the neighborhoods in context of the larger region.

Following are the general takeaways from that analysis that may play a role in Peoria’s changing grocery retail landscape. The analysis highlights that population changes, purchasing power, and retail grocery saturation are leading considerations.

Note: Figure numbers correspond with those in the referenced analysis

Population Changes

Tazewell County is growing at a much faster rate than Peoria County

Within the 10 County Intra-region, Peoria and Tazewell counties continue to be major population centers. From 1950-2010, both of these counties constituted approximately 50% of the regional population. Though Peoria has steadily continued to gain people (24% of the regional population in 1900 to 27% in 2010), Tazewell County’s population change has been more pronounced, from 9% of the regional population in 1900 to 20% in 2010.

The population has declined in the East Bluff and Southside neighborhoods

The East Bluff neighborhood experienced a higher population decline than the Southside neighborhood. From 2010 to 2016, within the Greater Peoria Region, the total population of the East Bluff neighborhood decreased by 3.4% (from 12,259 to 11,842 residents), compared to the Southside neighborhood, which experienced a 0.53% decrease in its overall residents (12,837 to 12,769 residents).

Population Pyramid for East Bluff and Southside Neighborhoods

The East Bluff and Southside Neighborhoods, like the Greater Peoria Region, have fewer men than women. The population pyramids for these neighborhoods are almost the shape of a “pyramid” - a broad base and narrow top, indicating a “growing and younger population;” East Bluff has more “working age group individuals” -30-34 years of age, compared to Southside, which has a growing population of “5 years and under” age group.

Purchasing Power

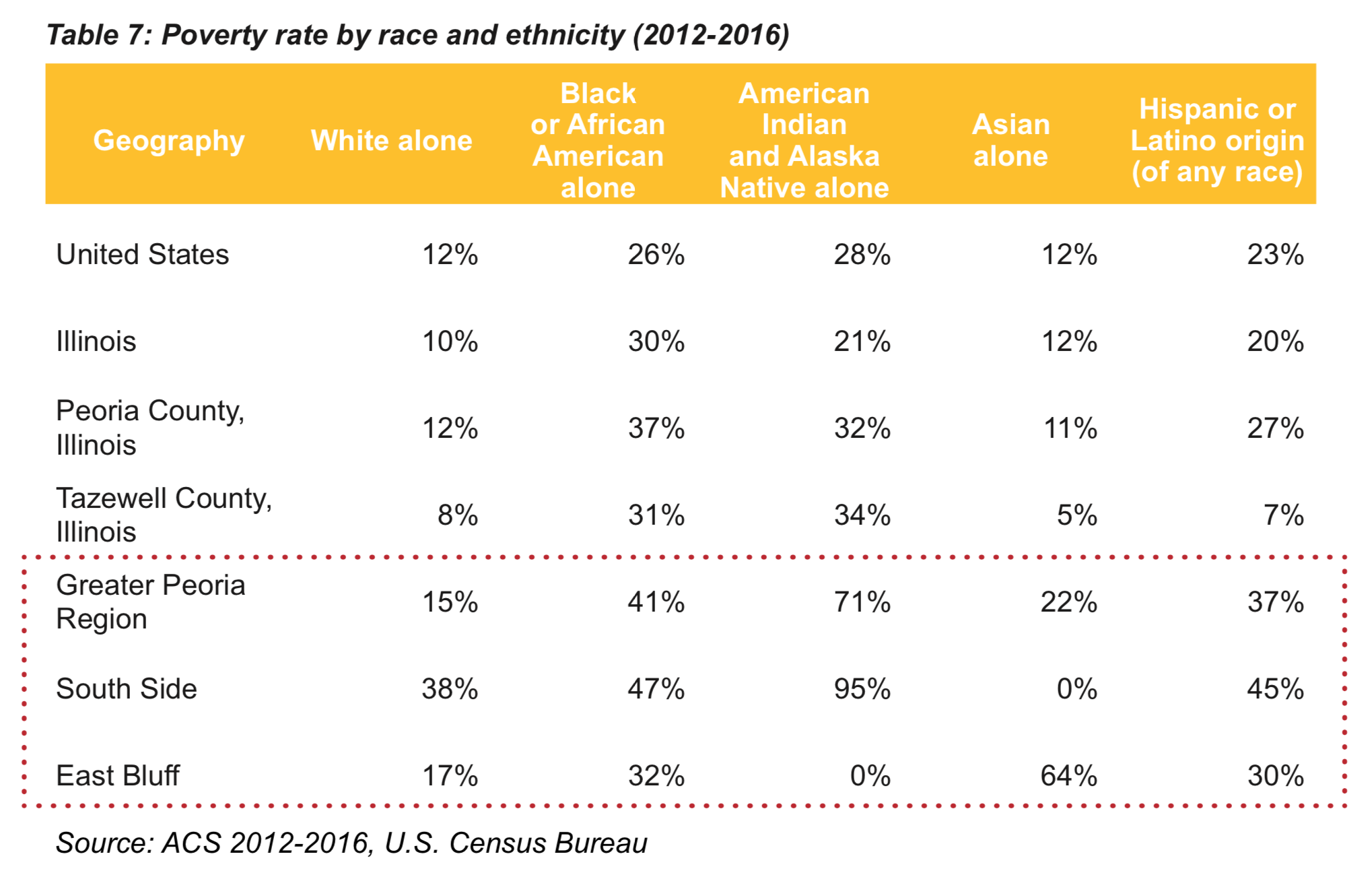

Median incomes lowest in Southside and highest in Tazewell County

In 2016, across all geographies (United States, Illinois, Peoria County, Tazewell County, the Peoria/East Peoria targeted study area, East Bluff, and Southside neighborhoods), the median income of Tazewell County residents at $60,178, was the highest.

Residents of the Peoria/East Peoria Study Area, East Bluff, and Southside neighborhoods had median incomes less than the national, state, and county averages. In 2016, the median income of Southside residents at $22,247, was a third of the median income of Tazewell County residents. Table 13 also shows that for almost the same number of households (approx. 4,500 total households), the median income of Southside residents was almost 40% less than that of East Bluff residents.

Concentration of poverty in Southside and East Bluff neighborhoods

The 10-county Greater Peoria Region had a poverty rate of 22.7%, higher than the national and state average. Approximately 45.1% of Southside residents and 23.2% of East Bluff residents had income below poverty level.

Across the region, children have higher poverty rates. Even though the overall poverty rate for the region is 22.7%, 34.3% of children under the age of 18 were living in poverty. Likewise, the poverty rates for children of East Bluff and Southside Neighborhoods are elevated as well—60.9% of South Side children under the age of 18 years of have the highest poverty rate compared with national, state, county and local averages.

By race, the highest poverty rates in the Greater Peoria Region were for American Indians and Alaska Natives (71.5%) and Blacks or African Americans (40.7%). Approximately 47% of all Blacks or African Americans in the Southside neighborhood had income below the poverty level. A third of all Blacks or African Americans in the East Bluff neighborhood had income below the poverty level, the highest for that area. For the Hispanic or Latina population within the Greater Peoria Region, 37.4% had income below the poverty level. Likewise, a third of all East Bluff’s Hispanic or Latina residents and less than half of Southside’s Hispanic or Latina residents had income below the poverty level.

High utilization of Supplemental Nutrition Assistance Program (SNAP) in Southside and East Bluff

SNAP is a federal program to supplement and improve nutrition needs of low-income people by increasing their food purchasing power. In fiscal year 2016, SNAP assisted nearly 44.2 million people; about 14% of the total U.S. population, about one in seven Americans.

Within the Peoria/East Peoria targeted study area, 21.6% (8,866) of all households received SNAP benefits, which is higher than the national (13%), state (13.3%), and county (Peoria at 14.1% and Tazewell at 9.7%) averages.

Likewise, about 42% of all Southside and 26% of all East Bluff residents received SNAP benefits, which is higher than the national, state, county, and local averages.

Of all households receiving food stamps, 65% of Southside and 58% of East Bluff residents were below the poverty level and 54% of South Side and 60% of East Bluff residents had children under 18 years of age.

Lower than average food expenditures in Southside and East Bluff

Table 14 provides a more detailed look at average estimated household spending on retail goods and services. As with the Household Budget Expenditures, spending in each category is indexed against the national average. The average expenditures in the food sub-categories in each geographic area mirror the estimates in the household budget expenditures table.

Within the Food category, spending in the 10-County Region is near the national average. The East Bluff and Southside are estimated in this category at 66% and 47% respectively. These levels are unsurprising given the household income profile of these areas in comparison to the U.S. national average household income.

Tapestry Segmentations

Tapestry segments are a classification of household types. According to ESRI, Tapestry Segmentation “provides an accurate, detailed description of America’s neighborhoods—U.S. residential areas are divided into 67 distinctive segments based on their socioeconomic and demographic composition.”

Each segment has a full profile that includes demographic information and market preferences. The segment profiles can be further explored at the ESRI Demographics website. This tool informs business planning to better understand consumer preferences and purchasing power in a given area. Below are the top Tapestry Segmentations with the study area.

Regional Study Area (10-county and Peoria/East Peoria): Rustbelt Traditions

The backbone of older industrial cities in states surrounding the Great Lakes, Rustbelt Traditions residents are a mix of married-couple families and singles living in older developments of single-family homes:

While varied, the work force is primarily white collar, with a higher concentration of skilled workers in manufacturing, retail trade, and health care. Rustbelt Traditions represents a large market of stable, hard-working consumers with modest incomes but an average net worth of nearly $400,000. Family oriented, they value time spent at home. Most have lived, worked, and played in the same area for years.

East Bluff: Traditional Living

For the East Bluff, the Traditional Living Segmentation ranked highest and is described as residents who live primarily in low-density, settled neighborhoods in the Midwest:

The households are a mix of married-couple families and singles. Many families encompass two generations who have lived and worked in the community; their children are likely to follow suit. The manufacturing, retail trade, and health care sectors are the primary sources of employment for these residents. This is a younger market—beginning householders who are juggling the responsibilities of living on their own or a new marriage, while retaining their youthful interests in style and fun.

Southside: Modest Income Homes

The Modest Income Homes Tapestry Segmentation tops the list in the Southside neighborhood. ESRI provides the following description:

Families in this urban segment may be nontraditional; however, their religious faith and family values guide their modest lifestyles. Many residents are primary caregivers to their elderly family members. Jobs are not always easy to come by, but wages and salary income are still the main sources of income for most households. Reliance on Social Security and public assistance income is necessary to support single-parent and multigenerational families. High poverty rates in this market make it difficult to make ends meet. Nonetheless, rents are relatively low, public transportation is available, and Medicaid can assist families in need.

Retail Grocery Saturation

It should be noted that the gap/surplus estimates and store location map have likely changed since the closures of grocery stores within the area. This section of the report was created with the most current data available in late 2018. Additional updates will be made when new data are available.

Gaps & Surplus in Retail Grocery

Where demand exceeds sales—when the spending of residents exceeds the amount purchased in a geography—leakage has occurred. This means that the demand in a given category is not totally satisfied within the geography and there is retail gap as residents of the geography are making some of their purchases of that good or service outside the geography’s boundaries. A retail gap may present the opportunity for business development.

When a greater amount of a retail good type is purchased within the geography than is demanded by residents of that geography a retail surplus has occurred. In this case, businesses within the geography have not only met local demand, but they have attracted spending from outside of the geography’s boundaries.

In the 10-county region surrounding Peoria, in 2017 there was an estimated retail surplus of $399 million for grocery stores and a retail gap of $23.1 million for specialty food stores.

For the Peoria/East Peoria area there was an estimated $10.7 million retail gap for grocery stores and a retail surplus of $3.3 million for specialty food stores.

In the East Bluff neighborhood in 2017 there was an estimated retail surplus of $19.5 million for grocery stores and a retail gap of $943,000 in specialty food stores.

In the Southside neighborhood in 2017 there was a retail gap of $3.4 million for grocery stores and a retail gap of $636,000 in specialty food stores.

It should be noted that these estimates have likely changed since the closures of grocery stores within the area.

Additional information about the methodology that ESRI uses to create the Retail MarketPlace Profile is available at the following link: https://support.esri.com/en/white-paper/3569

Grocery Store Locations

These map show the location of grocery stores and superstores within the study area. In total the analysis found eight grocers within the Southside neighborhood and four stores selling groceries within the East Bluff neighborhood. When analyzing a ring within 5 miles of the two neighborhoods there were a total of 44 grocery stores and five superstores.

Since the Kroger closures, a community member compiled this map of existing grocery and convenient store locations via an informal survey process. This map can be further developed and regularly updated to provide a current directory of area grocery stores.

Commuting Patterns

It’s important to note that the regional market is further impacted by the labor market. For the 98,622 workers who are employed in Peoria County, approximately 30% live in the City of Peoria, small percentages are from East Peoria, Pekin, Washington, and Morton, and 51% of workers coming into Peoria from the larger region. Daytime population increases by 15,759 workers.

Factors Supporting and Hindering Grocery Retail in the Impacted Neighborhoods

Factors supporting Grocery Retail

Net Job Inflow for the targeted study area of Peoria/East Peoria 20,717 workers who live in other areas are coming into the community to work

Market analysis illustrates gap in speciality food market as an opportunity

Strong preferences indicated by Grocery Store Access Resident Survey respondents for neighborhood market

Rustbelt Traditional tapestry segmentation with strong ties to the area

Limited access to fresh foods

Limited means for transportation

Growing population of “5 years and under” age group in Southside Neighborhood

In the South Side neighborhood in 2017, there was a retail gap of $3.4 million for grocery stores and a retail gap of $636,000 in specialty food stores.

Factors that may hinder Grocery Retail in the Impacted Neighborhoods

Concentrated poverty

Limited transportation alternatives

Loss in overall population

Saturation of the grocery retail market at the regional level

Lower than national averages in household budget expenditure for food (both food at home and food away from home)

Utilization of SNAP benefits higher than state and national levels

In the East Bluff neighborhood in 2017, there was an estimated retail surplus of $19.5 million for grocery stores (possibly changed following the Kroger closure).

Want to take a deeper diver into the demographic and market analysis? Find it on the resources page.